go back

go backThe Dynamics of India’s Aviation Industry

In recent years, India has emerged as one of the top three largest aviation markets, according to the International Air Transport Association (IATA). With an annual 8% increase in traffic over the next two decades, its fast-paced commercial growth can be attributed to domestic air travel, a young fleet, and other factors.

After the recent trip to the region, Dhruv Gupta, Business Development Manager at Magnetic Engineering & Magnetic Training, provides an overview of its highlights.

The current state of the market

Based on the last year’s air traffic, India is now the third-largest civil aviation market globally, with ~180 million passengers (136 M domestic, 44 M international). Throughout 2023, the industry generated an annual contribution of 53.6 billion USD to the local economy, underpinning 7.7 million jobs in the country.

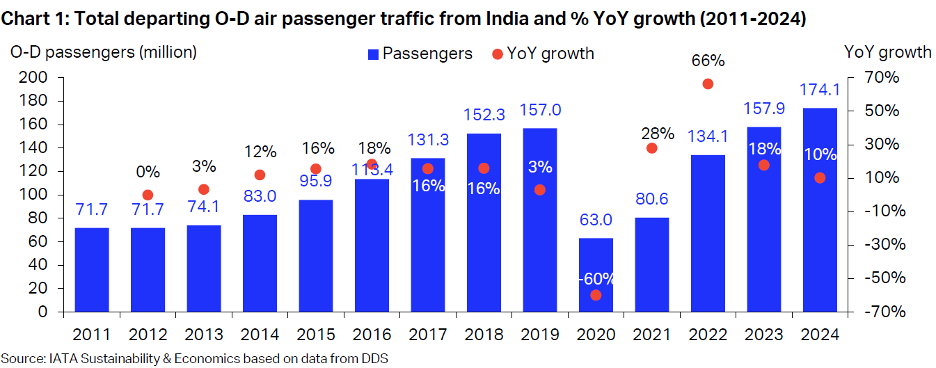

It’s also worth noting that between 2011 and 2019, India experienced an impressive double-digit average annual growth rate of 10.3% in air passenger Origin-Destination (O-D) departures. Following the disruption caused by the pandemic, in 2024, India’s traffic levels surpassed their 2019 level by 10.9%, marking a fourth consecutive year of double-digit growth.

“The aforementioned “growth spurts” signify the rapid development of the aviation market within India’s borders and beyond. From a personal perspective, that has also been notable while attending global industry events hosted locally, such as Airline Economics and others. They are still smaller in size, but the interest is certainly there as the major players are attending. The same confirmation has been received when meeting current and potential partners in 2025, with a focus on MROs and airlines.

To illustrate the scope, IndiGo alone has more than 2.5K flights a day. However, the regional maintenance capacity is not there yet, topped by the lack of infrastructure, so this in combination makes them rely on Europe and the US to fulfill the demand. For us, the established premise on the industry’s growth also corresponds business-wise. For example, since 2023, our EASA part 147 Training organization has seen a 30% increase in demand from our India-based customers across diverse technical training categories,” added Dhruv.

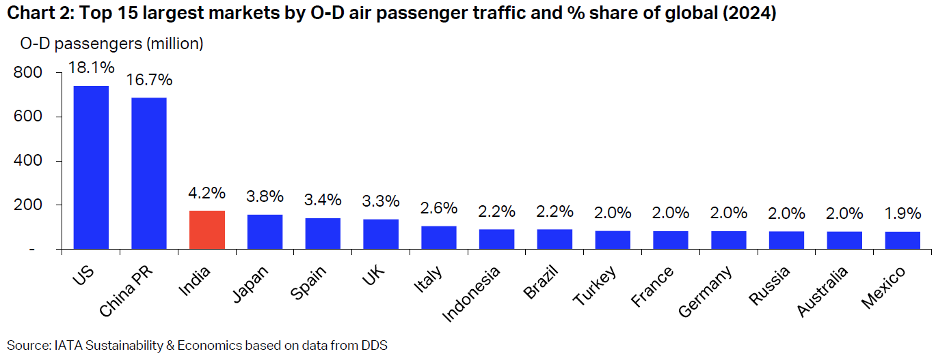

India now ranks as the third largest air transport market in the world in terms of departing O-D passenger traffic, behind the United States and China.

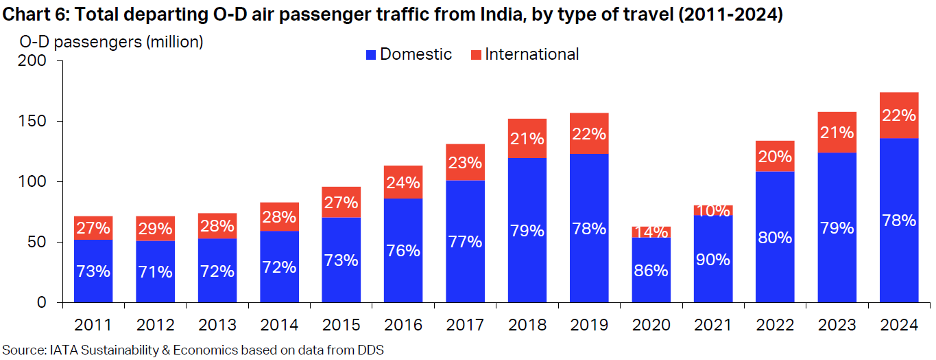

Of the 174.1 million passengers departing from an airport in India in 2024, more than 136.1 million flew domestically. Putting aside the pandemic disruption, the market share of domestic traffic has risen from around 72.9% a decade ago to almost 78.2% currently, reflecting the substantial network expansion undertaken by domestic carriers, notably IndiGo, as mentioned above.

Lastly, one more interesting and rather market-specific observation is that in such a large market, there are not many players. IndiGo holds a monopoly if we talk about the domestic market, which has almost 53.4% market share. If we look at the international market share, it is dominated by Air India, as it is the only airline with connections to Europe, Australia, the US, and Canada.

A comparative take on Europe

Both markets, India and Europe, differ significantly in terms of the market itself. Europe is already considered to be mature and saturated. India has been rapidly growing at a double-digit rate every year, but it still has low per capita air travel due to a significant gap in purchasing power. Consequently, airlines are competing with the vast rail network within India. Second, the business model in Europe is a mix of full-service and LCC; however, in India, as we saw earlier, the domestic market is dominated by LCC, with a share of almost 60%, while full-service carriers hold a relatively small share.

The EU has more relaxed laws regarding fifth freedom rights with many countries, whereas India only has bilateral air service agreements. Additionally, Europe’s infrastructure is well-developed, with multiple mega-hub airports, in contrast to India’s regional infrastructure, which is still in progress. However, it is developing fast, and the goal is to have 400 airports throughout India by 2047.

Finally, Europe operates on strong leasing markets, and airlines are listed on stock markets. Indian operators are heavily reliant on sale-leaseback arrangements and must prioritize strengthening their financial health due to high fuel costs and surcharges, as well as frequent, highly restrictive regulations and the influence of authoritative bodies.

Regional challenges and opportunities

Let’s start with an overview of which market-specific factors present potential opportunities.

Passenger Growth

– Young, physically active population together with the rising middle class = sustained demand

– Air travel use is low (~0.1–0.15 trips per capita vs. ~2 in Europe)

– Domestic travel is expected to grow ~10% annually; international ~15–20% by the data seen earlier

Aircraft & Fleet Expansion

– Over 1,500 aircraft on order (IndiGo, Air India, Akasa, etc.)

– India is now among the top global buyers of new aircraft

– Aging fleets offer room for upgrades, retrofits, and support services

MRO & Aerospace Manufacturing

– The government aims to make India an MRO hub (domestic market worth ~$2B) using its Make in India policy

– Incentives for OEMs and component suppliers to manufacture locally

– OEMs like Airbus, Safran, Boeing, and Rolls-Royce have expanded Indian footprints

From cultural nuances to the business landscape, here’s a list of challenges to consider when entering the Indian market.

Cost Sensitivity & Price Pressures

– Indian airlines operate on ultra-thin margins

– Intense price competition forces downward pressure on vendor pricing

– High ATF costs, lease dependency, and currency fluctuations squeeze profitability

Cultural & Relationship Nuances

– Business is relationship-driven, not purely transactional

– Decision-making can be more hierarchical and slower than in Europe

– Having established contacts among relevant governmental bodies are often needed to help speed up the processes and approvals

Regulatory Complexity, Bureaucracy & Dispute Resolution

– Lack of regulatory alignment

– Rules change slowly, and approvals (e.g., for leases, MROs, routes) can be unpredictable

– High customs duties and lack of GST on aviation fuel create cost burdens

– Contract enforcement and dispute resolution can be inconsistent

Key takeaways

Historically, the Indian market has been a challenging one for airlines, with numerous market entries and exits. Among the more notable recent bankruptcies are GoAir (2021), Jet Airways (2019), and Kingfisher (2012). Over the last two decades, more than 15 airlines registered in India have failed. Even though the market is not as stable, we still see new operators emerging, with a few notable examples, such as Akasa Air, which started operations in 2022 with B737 Max-type aircraft, and Fly91 in 2023 with ATRs.

Since the market is large, there is still ample room for new startup airlines, especially with the support of government initiatives like UDAN, which prioritizes regional connectivity as its primary goal. Continuous support for airlines and the development of new airports in regional parts of the country, as well as connecting them with major cities, are examples that demonstrate it’s still possible for new operators to enter the market and join the industry.

Similarly, trade-free zones in Hyderabad and Delhi, as well as GIFT City in Gujarat, serve as a signal for OEMs and lessors to establish a presence in the country, diversifying the aviation industry in India with more players in the market while driving down prices, thereby helping to sustain competition. OEMs have the advantage of these tax-free schemes, which makes India a more lucrative market for their establishment. As we can already see, the effects of these lessors, such as Avolon and Aercap setting up offices in GIFT City and Airbus and Safran setting up major facilities in the Hyderabad trade zones, all seem to be setting the stage for a growth trajectory in the foreseeable future.